I started calling online advertising a bubble in 2008.

I made “The Advertising Bubble” a chapter in The Intention Economy in 2012.

I’ve been unpacking what I figure ought to be obvious (but isn’t) in 52 posts and articles (so far) in the Adblock War Series. This will be the 53rd.

And it ain’t happened yet.

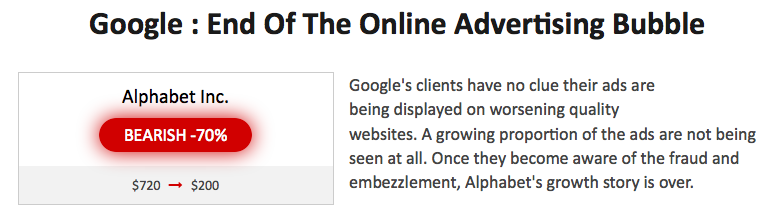

But, now comes this, from Kalkis Research:

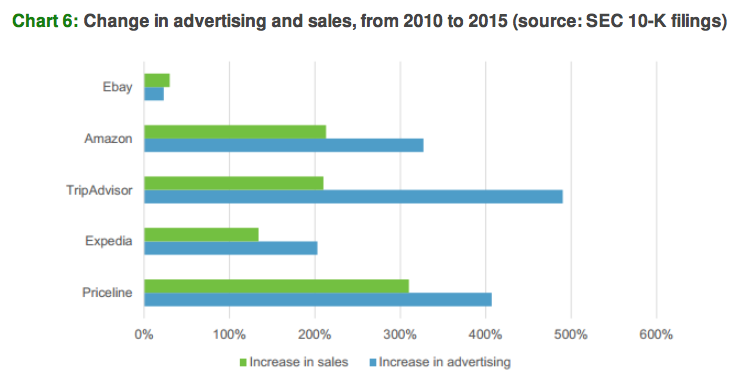

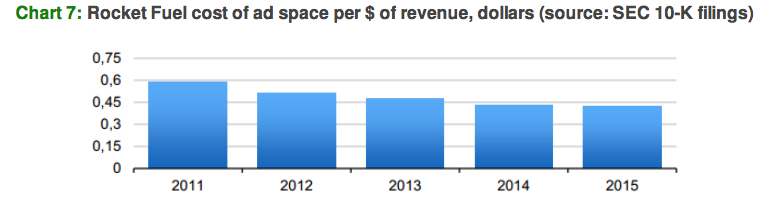

Some charts:

And here is their downbeat conclusion:

We are living through the latest stages of the online advertising bubble, as available high-quality ad space is shrinking, leading to a decline ad space quality, and a decline of ad efficiency. Awareness for fraud is growing, and soon, clients will cut their online ad spending, and demand higher accountability. This will destroy the high-margin market of automated reselling worthless ad space, and will force advertisers to focus only on prime publishers, with expensive ad space.

This is a re-run of the online advertising crash of the early 2000s, when the proliferation of banners and pop- ups destroyed any value these ads had (and led people to install pop-up killers, just like with ad blockers today)…

We estimate that the online advertising market has been artificially inflated since the end of 2013, and is much more mature than its pundits are claiming. 90% of Google’s revenues come from advertising. We expect Alphabet’s share price to go down by 75%…

A larger number of companies will be impacted, as a growing number of third-party tech giants are involved in the advertising play (Oracle, Amazon, Salesforce), and we expect the whole tech sector to be hard hit by the unwinding of the bubble…

Currently, January 2018 Alphabet puts with a strike of $400 are trading at around $8, for a 20x return should our scenario materialize.

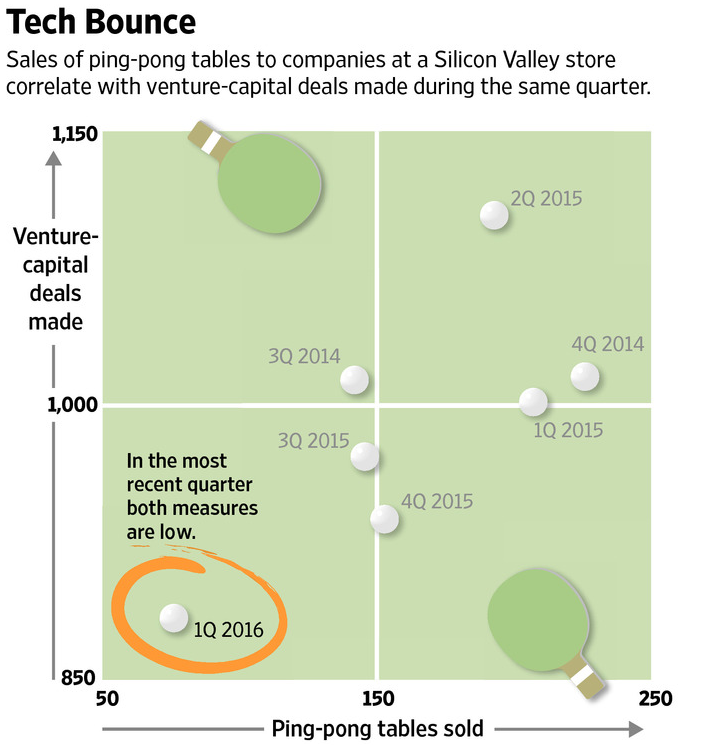

There are other signs. For example, a falling ping-pong table index:

GroupM, the “world’s largest media investment group,” also just published Interaction 2016, which is also bearish on adtech:

Advertisers and the entities that place their ads have always sought relevance and engagement; the consumer has chosen to set a higher bar. Advertisers and the buyers of media have a further responsibility.

Until now, we have assumed almost all data are worth having. But however much he gathers, no advertiser commands complete, continuous data. This creates a risk that the advertiser’s left hand may not know what his right hand is doing. A customer who has already made a purchase may be bombarded with redundant repeat ads wherever he roams: what we might call the phenomenon of “repetitive irrelevance.” Even worse, several advertisers may be sharing the same data and using performance-oriented media, multiplying the “repetitive irrelevance.” Tracking and targeting intended to make advertising welcome makes it a nuisance. It is dysfunctional. The advertiser damages his reputation and pays to do so.

This brief analysis suggests that a partial solution to adblocking is a combination of design, technology, common sense and the ability to establish the point, across channels and vendors, at which the application of a particular data point becomes the poison of marketing rather than the antidote to ineffectiveness.

The emphasis is mine. (Hey, I know boldface tends to get read and blockquotes don’t.)

There are other signs. Last May Business Insider said The ad tech sector looks an awful lot like a bubble that just popped. In June, The Wall Street Journal said adtech investment dollars are running dry. “These companies are struggling to even get meetings,” they said. In December Ad Exchanger called 2015 a “reality check” year for adtech.

Clearly the end isn’t near for Facebook or Google. Tony Haile, founding CEO of Chartbeat — and to me the reigning king of adtech moneyball — compares Facebook to the Sun, and everybody else to planets and other debris orbiting around it. One pull-quote: “It is Facebook that curates and distributes. It owns the relationship with the user, and decides what content the user sees and how many see it.” Meanwhile Google, which places a huge percentage of online ads (for itself and countless others), is said by Digiday to be exploring an “acceptable ads” policy obviously modeled on the one launched by Adblock Plus. And while ad fraud has been bad, AdAge reports that it’s down, dramatically: “analytics firm Integral Ad Science found a 20.9% decrease in both overall and programmatic ad fraud last quarter compared to the fourth quarter of 2015.”

Still, I’ve been told by one (big) adtech exec that his business is “a walking zombie” and that he’s looking toward “the next paradigm.” One of the biggest online advertisers told me late last year that they yanked $100 million/year out of adtech and put it into traditional advertising for one simple reason: “It didn’t work.” I have a sense that they are not alone.

Got any more examples? I want us to get as clear a picture as we can of the adtech edifice as it starts crumbling to the ground. Or not. Yet.

(Later…) Okay we have some:

- The Theory of Peak Advertising and The Future of the Web, by Tim Hwang and Adi Kamdar, October 9, 2013

- KMPG Media Tracker, which has a UK survey that says, “47 per cent of high earners say they’ll be using an ad blocker in the next six months, 59 per cent of 18-24 year olds say the same,” and “The group least likely to use ad blockers were the over 65s, at 36 percent.

- Are Peak Advertising Predictions Now Coming True? in Screen Media Daily (Thanks to Lionel Topper, below, all three of these.)

- At least one of Israel’s leading VC-backed adtech companies will be at best a shadow of its former self by the end of 2016, by Michael Eisenberg in Aleph.vc, January 13, 2016. (Thanks to Don Marti for that one.)

Leave a Reply